The U.S. economy saw job creation decelerate in October, confirming persistent expectations for a slowdown and possibly taking some heat off the Federal Reserve in its fight against inflation.

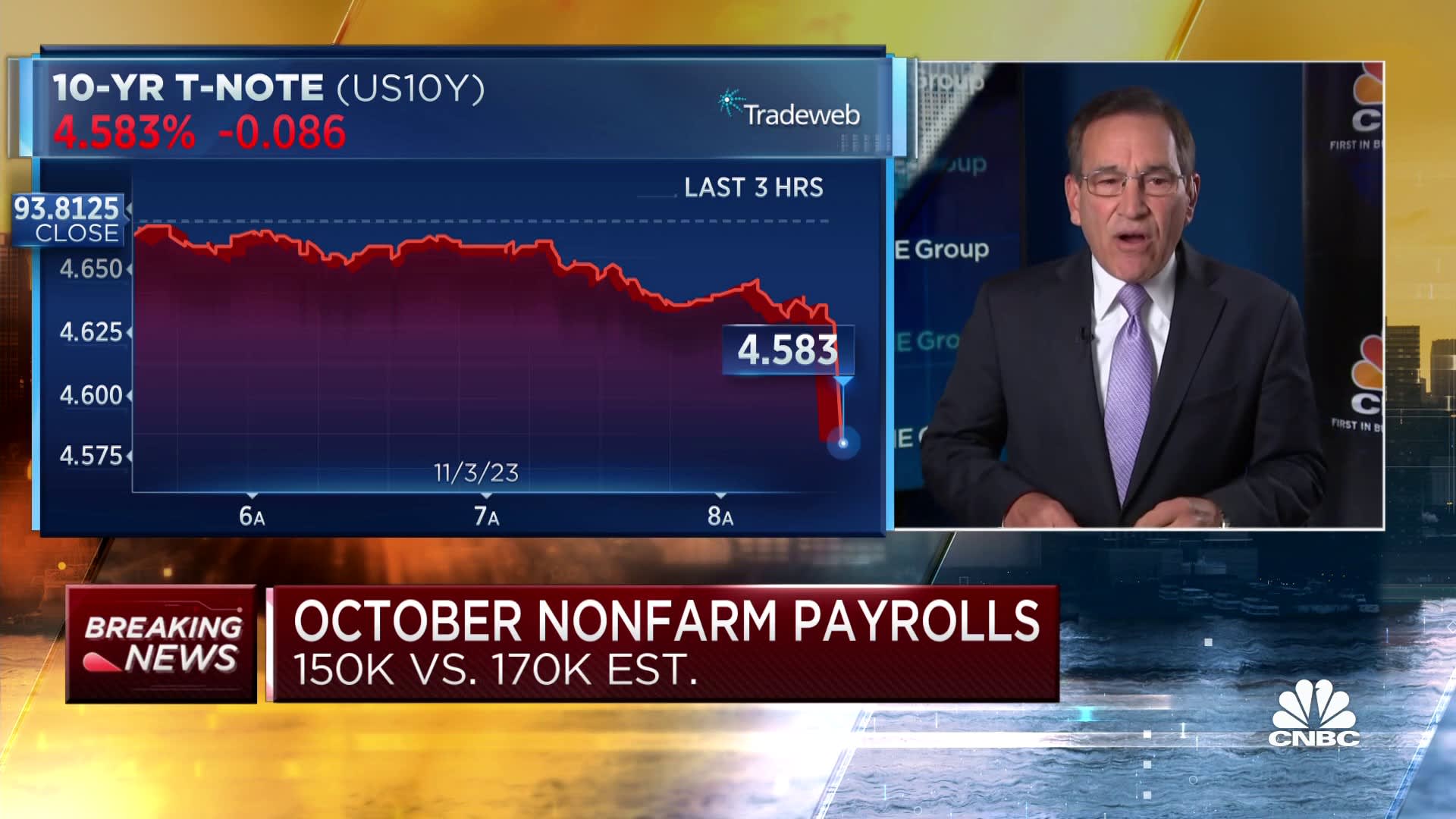

Nonfarm payrolls increased by 150,000 for the month, the Labor Department reported Friday, against the Dow Jones consensus forecast for a rise of 170,000. The United Auto Workers strikes were primarily responsible for the gap as the impasse meant a net loss of jobs for the manufacturing industry.

The unemployment rate rose to 3.9%, the highest level since January 2022, against expectations that it would hold steady at 3.8%. Employment as measured in the household survey, which is used to compute the unemployment rate, showed a decline of 348,000 workers, while the rolls of the unemployed rose by 146,000.

A more encompassing jobless rate that includes discouraged workers and those holding part-time positions for economic reasons rose to 7.2%, an increase of 0.2 percentage point. The labor force participation rate declined slightly to 62.7%, while the labor force contracted by 201,000.

“Winter cooling is hitting the labor market,” said Becky Frankiewicz, chief commercial officer at staffing firm ManpowerGroup. “The post-pandemic hiring frenzy and summer hiring warmth has cooled and companies are now holding onto employees.”

Average hourly earnings, a key measure for inflation, increased 0.2% for the month, less than the 0.3% forecast, while the 4.1% year-over-year gain was 0.1 percentage point above expectations. The average work week nudged lower to 34.3 hours.

The Fed uses wage data as one component of its inflation watch. The central bank has opted not to raise interest rates at its past two meetings despite inflation running well above its 2% target. Following Friday’s jobs data, markets further reduced the probability of a rate hike in December to just 10%, according to a CME Group gauge.

Markets reacted positively to the report, with futures tied to the Dow Jones Industrial Average adding 100 points.

From a sector standpoint, health care led with 58,000 new jobs. Other leading gainers included government (51,000), construction (23,000) and social assistance (19,000). Leisure and hospitality, which has been a top job gainer, added 19,000 as well.

Manufacturing posted a loss of 35,000, all but 2,000 of which came because of the auto strikes. Transportation and warehousing saw a decline of 12,000 while information-related industries lost 9,000.

“After years of incredible strength, the labor market could finally be slowing. The topline miss, plus downward revisions and higher unemployment, deliver a strong message to [Chair] Jerome Powell and the Fed,” said David Russell, global head of market strategy at TradeStation. “Further tightening is now highly unlikely, and rate cuts could be back on the table next year.”

In addition to the October slowdown, the Bureau of Labor Statistics revised lower its counts for the previous two months: September’s new total is 297,000, from the initial 336,000, while August came in at 165,000 from 227,000. Combined, the revisions took the original estimates down by 101,000.

Job creation skewed heavily to full-time workers, reversing a recent trend. Full-time jobs grew by 326,000, while part-time tumbled by 670,000 as summertime seasonal jobs wrapped up.

The report comes at an important time for the U.S. economy.

Following a third quarter in which gross domestic product expanded at a 4.9% annualized pace, even better than expected, growth is projected to slow considerably. A Treasury report earlier this week put expected fourth-quarter GDP growth at just 0.7%, and 1% for the full year 2024.

Fed policymakers have deliberately tried to slow the economy in order to tackle inflation. On Wednesday, the Fed’s rate-setting committee chose to hold the line for the second consecutive meeting after a series of 11 hikes since March 2022.

Markets expect the Fed is likely done raising, though central bank officials insist they are dependent on incoming data and still could hike more if inflation doesn’t show consistent signs of falling.

Inflation data has been mixed lately. The Fed’s preferred gauge showed the annual rate fell to 3.7% in September, an indication of steady but slow progress back to its goal.

Surprisingly strong consumer spending has helped propel prices higher, with solid demand giving companies the ability to charge higher prices. However, economists fear that rising credit card balances and increased withdrawals from savings could slow spending in the future.